Meta Platforms: Its Economics and Valuation

I come to bury Caesar, not to praise him.

(from William Shakespeare’s Julius Caesar, spoken by Mark Anthony).

Amidst a global stock sell-off, Meta Platforms’ Q2 earnings proved an excellent redoubt, reminding investors of the firm’s remarkable growth and profitability. If Mark Zuckerberg’s present dalliance with generative AI turns out to be a more expensive reenactment of his foray into the metaverse, the company will still be in rude health. There are few firms on the planet that can take the risks Meta can, and few are led by a founder as successful as Zuckerberg. Nevertheless, an analysis of its economics and price-implied expectations embedded into its current, $515.45/share stock price, reveals the most rose-tinted expectations. There is a little suggestion that Meta’s financial health is threatened, or that its competitive position is imperilled, rather, expectations implied by the stock price reveal downsides of 10-53%. Consequently, the company earns a “neutral” rating from me. This report should, one hopes, aid the reader in understanding Meta’s economics, while leveraging the accounting adjustments I make and my reverse discounted cash flow (DCF) model. I have also made my data completely accessible in an accompanying spreadsheet.

Meta’s Advertising Cycle

Competition between firms can also be described in Coasian language as competition between intra-firm and inter-firm organisation, between whether economic activities should be done within the firm, or by the market. Within firms, individuals, units and divisions compete and cooperate to maximise their individual payoffs. Nicolas Petit and Thibault Schrepel call these the macro, meso and micro levels of competition. Competition at the industry level forces changes within firms that result in a firm facing new competitors at the market level. Concretely, by way of example, each of Meta Platforms divisions compete and cooperate over resources, and at the market level, Meta enjoys a monopoly in social media networks, but faces fierce competition at the industry level, where it is part of the Attention Economy.

My framing of Meta is, I think, an improvement of the economic structuralism currently in vogue: it explains why Meta can at once be a monopoly in social media while facing clear competition from ByteDance’s TikTok, a short-form video platform, and Alphabet’s YouTube. From an economic point of view, that competition for attention at the macro level is measured in advertising dollars, which account for 98% of revenues. It could be said that Meta is, at the macro level, an advertising company, selling its ads on its apps, which are strewn across what Ben Thompson calls the “Social/Communications Map“.

The price of Meta’s ads is subject to the same laws of supply and demand that I recently showed govern S&P 500 returns. Ad impressions take the place of supply, and the price-per-ad that advertisers are willing to pay for user attention, is demand. Ceteris paribus, as ad impressions rise, price-per-ads decline, and vice versa. The chart below, inspired by Thompson, shows just this relationship, with year-over-year changes in ad impressions usually inversely correlated with average price per ad.

The best time for advertisers to invest in advertising on Meta is when the supply of ad impressions is rising as, all things being equal, this pushes average price per ad down, which has the effect of improving advertising returns and making Meta more attractive to advertisers viz. its competitors, as was the case in 2022. With average price per ad growing in the last three quarters, Meta is vulnerable to more cost effective competition, because prospective advertising returns are lower. Nevertheless, the advertising business remains very strong.

The Advertising Business is in Rude Health

In the business of internet advertising, Meta has been staggeringly successful. It is what McKinsey & Company call a “growth giant”: a business that has exceeded the S&P 500’s total returns to shareholders (TRS) as well as the growth in global gross domestic product (GDP), throughout its public life. Since 2011, Meta’s advertising revenue has compounded at nearly 34% per year, compared to nearly 4% for global GDP. Even in the last five years, Meta's advertising business has continued to grow at an astonishing rate, with revenues compounding at nearly 12% per year. To put that into context, according to Crédit Suisse’s “The Base Rate Book”, between 1950 and 2015, the median 5-year annual growth rate (CAGR) was 5.2%, and 6.9% of firms compounded revenues at between 15% and 20% a year, and only 3.8% of firms had a higher rate of growth than that band. Even as one of the largest firms in history, Meta remains exceptionally expansive. This is a firm of historic dimensions.

This pace-setting growth has occurred even as growth in the number of daily active people (DAP) using its apps has fallen below global GDP growth, compounding at 2.09% per year since Q4 2018. With 3.27 billion DAP in 2Q 2024, those who do not use at least one Meta app are either in China, underage, or are in the Asia-Pacific, or Africa, and as those regions become richer, their citizens will join Meta. Growth in Europe has stalled, and with current, almost hostile regulations1, Europe can no longer be seen as a source of growth but of economic rents, while in the United States, growth is fairly listless2. Again, it is important to see Meta and its competitive position from multiple levels: as a social media company, it is reaching the limits of what is possible, but as an advertising business, it is still full of potential. Betting against Meta's long-run growth prospects is, in many ways, a bet that businesses will not need to advertise.

As an entire economy has been built on top of Meta's apps, the appetite for digital advertising has not dulled, and Meta is by far the best way to reach customers from across the world. In this, Meta is stronger for Apple's App Tracking Transparency policy, and the emergence of TikTok, both of which forced a surge in capital expenditure to expand the company's artificial intelligence capacity. As Dave Wehner, Meta's chief strategy officer, said on the Q3 2022 earnings call,

We are significantly expanding our AI capacity. These investments are driving substantially all of our capital expenditure growth in 2023. There is some increased capital intensity that comes with moving more of our infrastructure to AI. It requires more expensive servers and networking equipment, and we are building new data centers specifically equipped to support next generation AI-hardware. We expect these investments to provide us a technology advantage and unlock meaningful improvements across many of our key initiatives, including Feed, Reels and ads. We are carefully evaluating the return we achieve from these investments, which will inform the scale of our AI investment beyond 2023.

The response to those threats was to increase capital expenditure from $19.24 billion in 2021, to $32.04 billion in 2022. In the last twelve months (LTM), capital expenditure is $29.85 billion, with the company signalling that capital expenditure for the year will be between $30 billion and $37 billion. Such has been the success of these measures that Zuckeberg remarked in the Q2 2024 earnings call,

...across Facebook and Instagram, advances in AI continue to improve the quality of recommendations and drive engagement. We keep finding that as we develop more general recommendation models, content recommendations get better. This quarter we rolled out our full-screen video player and unified video recommendation service across Facebook -- bringing Reels, longer videos, and Live into a single experience. This has allowed us to extend our unified AI systems, which had already increased engagement on Facebook Reels more than our initial move from CPUs to GPUs did. Over time, I'd like to see us move towards a single, unified recommendation system that powers all of the content including things like People You May Know across all of our surfaces. We're not there, so there's still upside -- and we're making good progress here.

In terms of capex/revenue, my measure of "capital intensity", capital expenditure has grown as a share of revenue and remains high, at 19.93%:

This spending has only served to extend Meta’s lead over its rivals -with Alphabet its only peer competitor-, improving its ad targeting and measurements and its content recommendation algorithms, in a world where it is harder to track users and, despite protests to the contrary, TikTok has shown that people want algorithmically surfaced content. In the Q2 2024 earnings call, Zuckerberg explained that,

So, let’s start: across Facebook and Instagram, advances in AI continue to improve the quality of recommendations and drive engagement. We keep finding that as we develop more general recommendation models, content recommendations get better. This quarter we rolled out our full-screen video player and unified video recommendation service across Facebook -- bringing Reels, longer videos, and Live into a single experience. This has allowed us to extend our unified AI systems, which had already increased engagement on Facebook Reels more than our initial move from CPUs to GPUs did. Over time, I'd like to see us move towards a single, unified recommendation system that powers all of the content including things like People You May Know across all of our surfaces. We're not there, so there's still upside -- and we're making good progress here.

Moreover, and this points to the widening lead, he said,

AI is also going to significantly evolve our services for advertisers in some exciting ways. It used to be that advertisers came to us with a specific audience they wanted to reach -- like a certain age group, geography, or interests. Eventually we got to the point where our ads system could better predict who would be interested than the advertisers could themselves. But today advertisers still need to develop creative themselves. In the coming years, AI will be able to generate creative for advertisers as well -- and will also be able to personalize it as people see it. Over the long term, advertisers will basically just be able to tell us a business objective and a budget, and we're going to go do the rest for them. We're going to get there incrementally over time, but I think this is going to be a very big deal.

Supporting and Investing in Growth

Maintenance spending is often conflated with depreciation and amortisation, but this neglects the profound importance of technological obsolescence, especially in our age of rapid technological change and so, maintenance spending cannot simply be equated to depreciation & amortisation expense, which may overestimate the future economic life of long-term operating assets white underestimating the periodic capacity costs that must be incurred to sustain present revenues. Similarly, during inflationary periods, capital expenditures costs increase, so that depreciation, which is set at historical costs, understates maintenance costs, whereas in deflationary periods, capital expenditure costs decline, overstating maintenance costs. Moreover, the greater the rate of technological obsolescence and inflation, the less money can go into growth spending. The accounting adjustments that I have made to Meta’s reports allow me to attempt to better capture what the firm’s maintenance spending is. In that vein, in order to understand the magnitude and evolution of maintenance spending on tangible assets, I have used a method developed by Venkat Peddireddy in his PhD thesis, "Estimating Maintenance CapEx"3, to estimate Meta's maintenance spending, and so I:

...compute cumulative capacity cost as the sum of D&A expense, asset write-downs, loss on sale of assets, goodwill, and intangible asset impairments over the last five years (t-4 to t). The cumulative capacity costs is then divided by sales cumulated over the same period resulting in an average firm specific estimate of the cost of long-term operating assets required to generate a dollar of sale, which I refer to as “Capcost_ratio”. To compute the dollar amount of maintenance capex for the current year, I multiply the Capcost_ratio with the current-year sales. This measure uses the firm’s most recent information from the last five years on the loss of value in long-term operating assets to estimate an approximate value of maintenance capex required to sustain the firm’s current revenues.

The result is in the chart below:

The most obvious point is that the smoothed measure of maintenance capex has been lower than depreciation and amortisation expense since 2022. That year, in its 10-K, Meta said the following:

In connection with our periodic reviews of the estimated useful lives of property and equipment, we extended the estimated average useful lives of a majority of the servers and network assets from four years to 4.5 years, effective the second quarter of 2022, and further extended the useful lives to five years effective the fourth quarter of 2022. The changes in estimated useful lives were due to expected longer refresh cycles in our data centers. The financial impact of the changes was a reduction in depreciation expense of $860 million and an increase in net income of $693 million, or $0.26 per diluted share for the year ended December 31, 2022. The impact from the changes in our estimates was calculated based on the servers and network assets existing as of the effective dates of the changes and applying the revised estimated useful lives prospectively.

This was part of a larger trend in Big Tech that Stephen Clapham discussed in the wake of 2023 accounting policy changes. What this measure of maintenance capex suggests is that the rate of technological obsolescence is slower than Meta, among other Big Tech firms, estimated, and that the real economic burden of maintaining its tangible assets is lower than the firm's depreciation & amortisation expense. This over-depreciation shows that more capital is flowing to growth than the depreciation and amortisation expense suggests.

Here, I have to pose a paradox. In Michael J. Cooper, Huseyin Gulen and Michael J. Schill's paper, "Asset Growth and the Cross-Section of Stock Returns", they say,

One of the primary functions of capital markets is the efficient pricing of real investment. As companies acquire and dispose of assets, economic efficiency demands that the market appropriately capitalize such transactions. Yet, growing evidence identifies an important bias in the market’s capitalization of corporate asset investment and disinvestment. The findings suggest that corporate events associated with asset expansion (i.e., acquisitions, public equity offerings, public debt offerings, and bank loan initiations) tend to be followed by periods of abnormally low returns, whereas events associated with asset contraction (i.e., spinoffs, share repurchases, debt prepayments, and dividend initiations) tend to be followed by periods of abnormally high returns.1 In addition to these long-run event studies, other work documents a negative relationship between various forms of corporate investment and the cross-section of returns. For example, capital investment, accruals, sales growth rates, and capital raising are found to be negatively correlated with future returns.

Meta has defied the gravitational pull of asset growth effects because the Internet Revolution and the possibilities it opened up to successful digital firms were so gargantuan, and many of its big bets, such as the investments in NVIDIA's GPU's that drove the surge in growth capex, have proven prudent, value-creating rather than value-destroying. Meta's bet is that there will be no normalisation of its returns, and that AI will prove a value creating rather than value destroying proposition. Yet, there are reasons for doubt, as Goldman Sachs' outlined their report, "Gen AI: too much spend, too little benefit?".

The most obvious source of rational doubt is that the long-run trend of Meta's capital intensity is rising, and that as capital intensity rises, the depreciation and amortisation expense will rise, probably triple4, eroding gross profits, as maintenance capex increases, perhaps tripling as well, widening the invested capital base, the net effect of which will be, all things held constant, to cause ROIC to decline, rather than rise. Meta will be aware of this, their bet is that there will be a surge in revenue that will at least counteract these effects. The trouble for Meta is that, at present, it has no meaningful ways to reap an immediate payoff from its AI investments, so near-term declines in NOPAT and ROIC cannot be dismissed.

To estimate Meta’s maintenance spending on intangible assets, I have borrowed a method developed by the accounting professors, Luminita Enache and Anup Srivastava, in their paper, “Should Intangible Investments Be Reported Separately or Commingled with Operating Expenses? New Evidence”. They cleave selling, general & administrative (SG&A) expenses in two: research and development (R&D) and advertising, on the one hand, which are classed as intangible investments, and “Main SG&A”, what are “SG&A expenditures other than R&D and advertising”, and are “matched with current revenues in a regression estimated by industry and year”, on the other. Main SG&A is further cleaved into “Maintenance Main SG&A”, which supports current operations, and “Investment Main SG&A”, which is the discretionary spending that is associated with future earnings. There is no clean way to calculate the investment and maintenance portions of R&D and Main SG&A, so, what I have done is to use the industry investment portions found by Ange Iqbal, Shivaram Rajgopal, Anup Srivastava, and Rong Zhao in their paper, "Value of Internally Generated Intangible Capital". According to their findings, 71% of R&D and 59% of Main SG&A, was dedicated to investment purposes in the communications industry. Not only is my use of a base rate a blunt tool, it is also undermined by my own estimate of advertising expense for the LTM, my assumption that advertising expense also has a 71% investment portion, and by the fact that "communications" is the closest to an industry I could place Meta in in Fama-French's industry classification. The reader may find more intelligent ways to deal with this problem. That aside, I calculate Intangible investments, which is the sum of Investment R&D, Investment Advertising and Investment Main SG&A; and Maintenance SG&A, which is the sum of Maintenance R&D, Maintenance Advertising Maintenance Main SG&A5:

Investment R&D is by far the most important category in the firm's SG&A, nearly tripling in size since 2019, along with maintenance R&D. In the LTM, Meta spent $42.48 billion on intangible investments compared to $20.65 billion on maintenance costs. The table below provides a breakdown of Meta's estimated intangible investments and maintenance SG&A costs:

Meta is behaving very much like a younger, focused firm, betting on growth rather than maintenance, with the bet that this investment spending will be compensated for by a rise in revenue and drive future NOPAT growth. Now, Meta is making a bet that its AIs will enrich user experiences, grow the economy of businesses built on Meta's products, make it easier to target ads and recommend content, allow Meta to create ads for its customers, and so enrich its hardware that Reality Labs products will become mainstream, turning the metaverse into a value creating bet.

Meta's Extraordinary Profitability

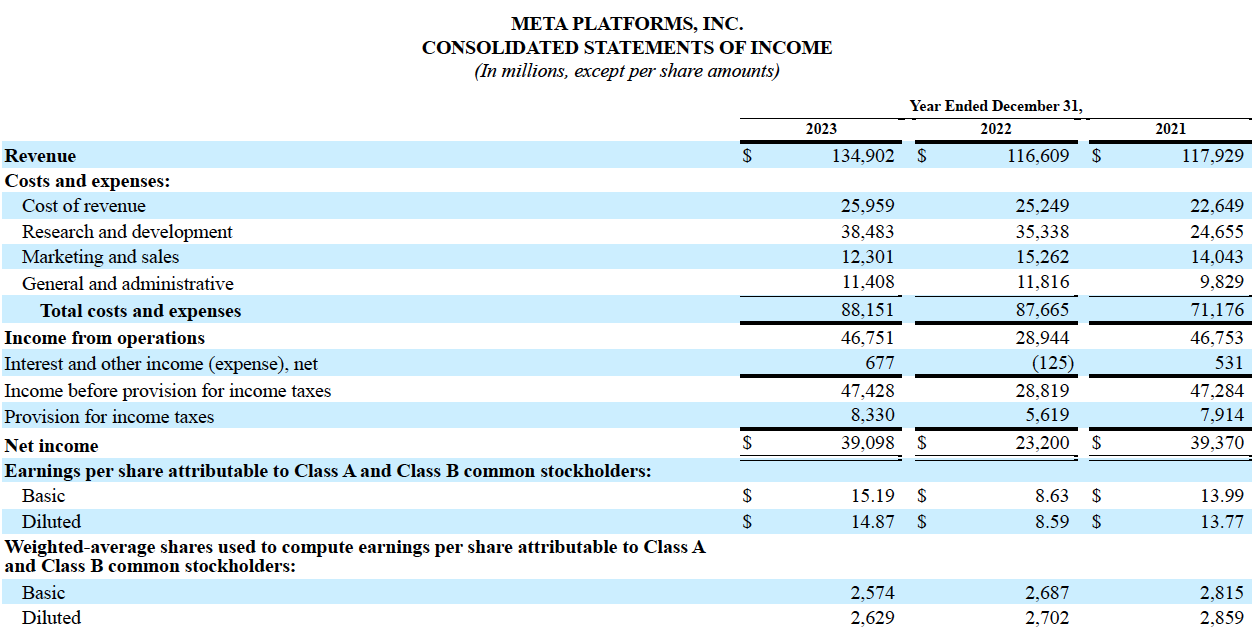

Meta has not only grown, it has done so while being remarkably profitable. Since its initial public offering (IPO) in 2011, Meta has only known profitability, with 2022 being the sole year in which the growth of its revenue and net operating profit after tax (NOPAT) have been checked. Since that controversial IPO, NOPAT has compounding at 32% a year. Again, even in the last five years, Meta has continued to set a blistering pace, with NOPAT compounding at 12.27% per year. After the App Tracking Transparency recession of 2022-2023, and the challenge posed by TikTok, Meta has emerged, in terms of raw numbers, stronger than ever: in the LTM, revenue is up 11% from 2023, within touching distance of $150 billion, and NOPAT is up 23%. On the entire planet, there are perhaps just five or so firms that combine this level of growth and profitability.

In an age in which many investors have wrongly assumed that merely being a platform or aggregator is enough to enjoy "winner-take-all effects", what Jonathan A. Klee has aptly called the "platform delusion", Meta has proven to be the real deal. Its success, built on a fortuitous timing that made a mockery of first-mover advantage; true network effects; a maniacal pursuit of customer satisfaction, or, if one likes a more cynical turn of phrase, enhancement of customer captivity6; and intelligently copying from rivals and buying out serious competition7, continues. Although Meta has been knocked out of the serious acquisitions business, its growth and profitability is unflagging. I would argue that, given how many M&A deals are value-destroying, Meta is better off for not being able to buy rivals.

It should be said that Meta's GAAP net income has, since 2021, tended to understate its true profitability. In the LTM, the degree of understatement is about $2 billion. Without careful accounting adjustments, one would have a far more "pessimistic" view of Meta's financial health.

Meta's NOPAT margin has averaged 30.01% from 2011 to the LTM, with 2022, its annus horribilis, having a NOPAT margin of 27.21%. Meta's invested capital turns (revenue/average invested capital) has averaged 1 across its lifetime, although it has fallen each year since 2021, from 1.18 to 0.96, indicating eroding balance sheet efficiency. Given that,

ROICt = (Invested Capital Turnst) * (NOPAT Margint)

where ROICt is the return on invested capital at time t, Invested capital turnst the invested capital turns at time t, and NOPAT margint the NOPAT margin at time t, it is not an imaginative leap too difficult to make for the reader to see that Meta's ROIC has been fairly stable, dipping violently just once in its history, in 2014, when it fell from 28% in 2013 to nearly 13%. In the LTM, ROIC is just over 34%, averaging 31.54% across its public life.

Meta has generated positive free cash flow (FCF) in every year since 2015, compounding FCF by 31.9% a year since then and even in the last five years, FCF continues to grow at a blistering pace, compounding by 36.5% a year. From a dividend point of view, there is a great deal of safety in the firm's dividends. That FCF, however, as a function of the firm's valuation, has a yield of just 2.96%, which get s a neutral rating from me8.

Capital Allocation

If there is a chart which Zuckerberg and his management team should be proud of, it is the above, which shows the economic profits earned by Meta since 2011. The fundamental principle of capital allocation is to engage in activity that earns a return on invested capital greater than the cost of that capital, and the dollar value of thais economic profit. Yet, for a company that is demonstrably so successful at value creation, it is curious just how little is said of capital allocation. Surprise recedes to understanding when one learns that as early as Meta's 2012 statement of intent, Zuckerberg was at pains to explain that,

Facebook was not originally created to be a company. It was built to accomplish a social mission — to make the world more open and connected.

Nowadays, it is the fashion for tech entrepreneurs to proclaim that they are pursuing some great mission for human civilisation, but, this is an early theme that I think has to be treated seriously, and which is important in understanding how Zuckerberg sees his body of work. Zuckerberg was clear in stating that Facebook was primarily concerned with its social mission, the services it was building, and the people who used it. In an age of cynicism, it is easy to pass over that statement without comment. This may seem naive, but, even if Zuckerberg was the world’s most sophisticated liar, those "lies" are the cornerstone of Meta’s culture and certainly the people who work for him believe the message he has communicated and soon enough, one believes what one repeats. So, it is irrelevant if he is a cynical liar or a a fervent believer, the effect, over time, is the same. Furthermore, in harmony with John Mearsheimer’s theory of lies, I believe that it is virtually impossible to build an entire organisation of sophisticated liars, so the words that a leader says, rather than what they secretly believe, are more operationally significant. The sophisticated liar is bound by his lies. I think it it right to say, without straining into the realm of unprovable psychobabble, that since that statement of intent, Zuckerberg has shown himself to be “el hombre de las dificultades”9, a man who loves great challenges, to hunt big elephants. This is a necessary prelude to understand why Zuckerberg has not always made the most optimal decisions, from a pure value creation perspective, whether it is in the share buyback strategy Meta has, or, in his decision to pursue the metaverse, where a more Buffettian approach may have been to spread his bets, or, begin issuing dividends earlier than he did. The organising principle governing Zuckerberg's actions is not value creation per se, but the building of great things. When the bets make sense, the distinction is meaningless, when the bets do not, which is rare for Zuckerberg, whether it is with the metaverse or perhaps even with artificial intelligence, the distinction leads to value-destroying actions. It should also not be surprising that very obvious errors in capital allocation are not addressed.

The Uses of Capital

Meta's capital is deployed into its business through capital expenditure, changes in its operating working capital, mergers and acquisitions, research and development (R&D), and to its cash claim holders through cash dividends, share buybacks, and debt repayment.

As I said earlier, I think it is correct to say that there is a de facto ban on major acquisitions by Meta, such that when there was talk of TikTok going up for sale, the most obvious candidate-acquirer, Meta, was not in the conversation. Since around 2016, acquisitions have not been a major element of the company's capital deployment. So, while recognising the fantastic work done by the company in acquiring and scaling and maintaining Instagram and WhatsApp, and questioning the Oculus acquisition, I will say nothing more about Meta-as-acquirer: the company is unlikely to make a meaningful acquisition in the near-term. I think debt repayment is relatively straightforward. Having already discussed Meta's capex, I will focus on two things: Meta's cost discipline, which seems to be the closest it has come to articulating a capital allocation philosophy; and its buyback policy.

A Necessary Cost Discipline

Meta's commitment to "cost discipline" is both admirable and condemnatory. Puritan finger wagging aside, the "year of efficiency" announced last year has indeed ushered in a more disciplined approach to costs. Cost discipline is part of a new section in the firm's reporting, "Investment Philosophy", first reported in its 2023 annual report, in which it said,

We expect to continue to build on the discipline and habits that we developed in 2022 when we initiated several efforts to increase our operating efficiency, while still remaining focused on investing in significant opportunities.

Total costs and expenses have risen just 3.22% between the LTM and 2023, compared to a rise of just 0.5% for the period prior. The post-2022 period has witnessed the slowest rate of costs and expenses growth in the firm's entire public life.

It is likely that, even without the App Tracking Transparency Recession, Meta would have had to take a more disciplined approach to its spending. Given that Meta does not have any meaningful marginal costs, slowing revenue growth does not automatically lead to lower cost of goods sold, so a deceleration has to be met by a more disciplined approach to expenses in order to forestall a decline in NOPAT margins. The App Tracking Transparency Recession merely increased the pressure on to be more disciplined, as NOPAT margins and invested capital turns plunged toward normalcy. Nonetheless, with near-term revenue growth unlikely to hit lifetime averages again, cost discipline is the new sine quo non.

The Buyback Policy

Meta's buyback policy is a gift-giving policy for the benefit of sellers. 2022 remains the only year in which the company has bought back its shares when its year-end closing price, which tracks the average price the firm paid for shares, was lower than its economic book value (EBV)10. 2018 was the only other year in which Meta bought back its own shares at a reasonable price-to-EBV, which in that year was 1.14 at year end. Meta is not a unique sinner in this regard, often, companies do seem to purchase their own stocks without any sense of the intrinsic value of the business, and, tend to buy shares on market highs rather than market lows. Indeed, as the table below shows, in 2022, Meta reduced its buybacks by 37%, rather than increasing it, and in the LTM, share buybacks have risen even as the company's valuation is at its greatest dislocation to its EBV since 2017. Management's unwitting largesse rewards sellers with the capital of continuing shareholders.

The main success of the buyback strategy in the 2017 and 2023 era, where it spent $117.86 billion on share repurchases, has been to reduce the number of shares outstanding between by 12.3%, although Meta still has 7% more shares outstanding than it did when it went public in 2012. This suggests a rather elementary approach to share repurchases as simply being about giving existing shareholders a bigger stake of the pie, without considering whether the price at which shares were being bought was attractive. A more considered approach would have had Meta greedily buying-up its shares in 2018 and 2022, and engaging in the most abstemious fasting in the other years. Meta does not seem to have a sense of its own intrinsic value.

Reverse DCF Reveals Rose-Tinted Market Expectations

Using my reverse DCF model, we can uncover the expectations implied by the current stock price of $515.45. In order to justify its current price, Meta must grow revenues by 13.6% a year for the next 14 years, while maintaining a 35.95% NOPAT margin, and compounding invested capital by 12.16% a year. In that scenario, Meta would earn $961 billion in revenue, nearly thrice Alphabet's LTM revenue. This scenario also implies that Meta would average a ROIC of 40.88%, compared to its lifetime ROIC average of 31.4%. Meta last had a ROIC greater than 40% in 2018. At the end if its competitive advantage period (CAP), Meta would earn a NOPAT of $345 billion. This is the -nothing-goes-wrong scenario. The reader can see how I solved for this in my attached spreadsheet, under the sheet titled, "Price-Implied Expectations".

If, however, NOPAT margins are 31.7%, while the pattern of growth and investments remains the same, then Meta is worth $462.32 per share, a downside of 10% from the current price. In this scenario, Meta averages a ROIC of 36%, above its 5-year average of 33.3%, and earn a NOPAT of $304.7 billion at the end of its implied CAP. The reader can see how I solved for this in the sheet named, "Reverse DCF (Pessimistic Case 1)".

If, rather than just lower NOPAT margins, Meta's growth does not match revenue expectations and looks more like it's 3-year compound annual growth rate of 8.3% per year, then Meta is worth $238.52 per share today, a 53% downside from its current share price. Under this scenario, Meta would enjoy a ROIC of 34%, while compounding NOPAT by just over 4% a year, attaining a NOPAT of $156 billion by 2038.

The important thing about testing the price-implied expectations in Meta's share price is that these are, to my mind, all plausible scenarios. While Meta's engines are well capable of going on the kind of run implied by expectations, the most modest and plausible of dips in performance open the door to steep declines in value.

- Mark Zuckerberg and Spotify CEO, Daniel Ek, said in a recent open letter, "The stark reality is that laws designed to increase European sovereignty and competitiveness are achieving the opposite. This isn’t limited to our industry: many European chief executives, across a range of industries, cite a complex and incoherent regulatory environment as one reason for the continent’s lack of competitiveness." ↩︎

- At the app level, the picture is more nuanced: for example, WhatsApp is growing in the US and Threads, less an app than a feature of Instagram's, is growing globally. The future is less about growing headline DAP or monthly actives, than about introducing the current pool of DAP and monthly actives to new set of apps and features. ↩︎

- Mauboussin and Dan Callahn’s paper, “Underestimating the Red Queen”, gives an excellent discussion of the limitations of Peddireddy’s method. ↩︎

- In his substack, "Big Tech Capex and Earnings Quality", John Huber makes a similar point. ↩︎

- Some might feel that these expenses should be capitalised. However, capitalising expenses does not impact free cash flows, and has minimal effects on a firm's ROIC, and may even hide a firm's economic travails. The process is also rife with uncertainty: for how many years should one capitalise expenses, and from when should one start? ↩︎

- In 2017, Zuckerberg explained that, "I think the strategy of Facebook is to learn as quickly as possible what our community wants us to do.” ↩︎

- The Federal Trade Commission (FTC) in their 2021 complaint, quoted Zuckerberg in a 2008 email, saying, "it is better to buy than compete.” ↩︎

- Very unatractive = <-5%, unattractive = -5%<-1%, neutral = -1%<3%, attractive = 3%<10%, and very attractive = >10%. ↩︎

- Spanish for "a man of difficulties”, which is what Venezuelan revolutionary, Simón Bolívar, referred to himself as. ↩︎

- Michael Mauboussin describes EBV as "The 'steady state' value of the firm, or the value of the firm assuming no incremental value will be created. It equals the company’s most recent net operating profit after tax (NOPAT) capitalized by the company’s weighted average cost of capital mi- nus debt. A price-to-economic-book-value ratio of 1.0 suggests the market expects no value creation. Any ratio above 1.0 assumes value creation and anything below 1.0 assumes value destruction." ↩︎