Companies create reserves in anticipation of probable future costs or losses whose amounts can be reasonably estimated, as happens with inventory reserves and loan-loss provisions, or, in order to ensure comparability across accounting methods as happens with LIFO reserves.

While operational excellence should be the lodestar guiding managers, there is a great temptation to use reserves to manage earnings. In order to ward off the effects of earnings management, ensure comparability across business, and reveal timing of recurring cash flows from operations, the change in LIFO reserves, other inventory reserves and loan loss reserves year-over-year are added to my calculation of net operating profit after tax (NOPAT).

The worries expressed in my short note on the change in reserves, pertain to the balance sheet as well, with managers well capable of adulterating asset values through the innocent exercise of the discretion that the rules allow. Reserves are added back to assets as part of my invested capital calculation.

Taxes incorporate operating, non-operating and financing items. One wants to assess the core operations of a business, free of any financing effects, in order to estimate net operating profits after tax (NOPAT), and so, one must break off operating taxes, from taxes on non-operating accounts, and other non-operating taxes. This gives us the taxes the firm would pay if it only engaged in its core activities and was wholly equity financed.

I start with reported provision for income taxes or income tax expense, and then subtract the change in the deferred tax account in order to convert taxes from an accrual to cash basis. When a company pays less in cash taxes than it reports in book taxes, it earns a deferred tax liability, a source of cash, and when it pays more in cash taxes than it reports in book taxes, it earns a deferred tax asset, a use of cash. The deferred tax account can be found on the balance sheet, but when they are not separately detailed, the relevant information can be found in the cash flow statement under the “Cash flows from the operating activities” section, as part of the adjustments to reconcile net income to net cash provided by operating activities; or, it can be found in the footnotes.

Then, I unlever cash taxes by adding back the debt tax shield from from net interest expense and operating, variable and not-yet commenced leases. This is done by multiplying the debt expense by the marginal tax rate, and adding the sum to cash taxes. Finally, I reverse the impact other non-operating accounts. Where there is information on tax benefit of non-operating items, with pre and post-tax values given, I reverse the impact of that as well. This process gives us an estimate of cash operating taxes.

This whole process can be seen in the example below in which I calculate Diamond Hill’s cash operating taxes.

These are the result of currency revaluations or devaluations and do not appear on the face of the income statement. These currency fluctuations force firms to assume non-recurring charges or gains. An example is the $12 million Tesla gained in 2013 when the Yen’s plunge reduced Tesla’s Yen-denominated liabilities. David Trainer, the CEO and founder of New Constructs, notes that,

The Bolivar Fuerte was adopted as the national currency of Venezuela in 2008. Companies operating in Venezuela must obtain government approval to exchange Bolivars to US Dollars at the official exchange rate. Effective January 1, 2011, the Venezuelan government established a fixed rate of 4.30 per dollar. Again, effective February 13, 2013 the currency was further devalued to a rate of 6.30 per dollar. This change caused many companies to take large charges on the remeasurement of their Venezuelan operations for their 2013 fiscal years. Such a charge is a one-time, non-operating expense and is not indicative of the operations of the company.

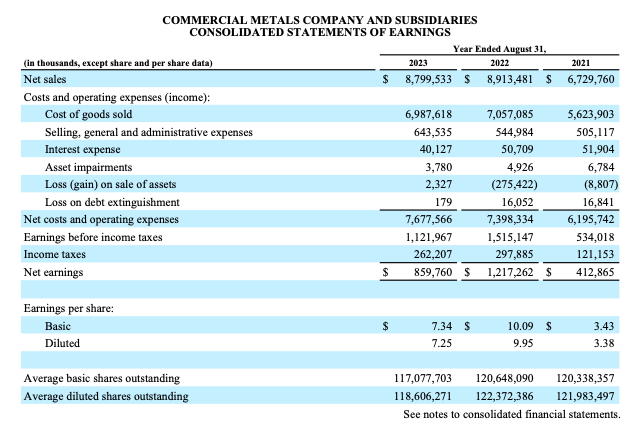

Reported net non-operating charges and gains are those non-operating items reported on the face of the income statement. According to the paper, “Core Earnings: New Data and Evidence” by Ethan Rouen, Eric So, and Charles C.Y. Wang, they are “similar in magnitude… to those reported off the face of the income statement”. Examples of such items are interest expense/income, minority interest income, preferred dividends, asset impairments, and losses on debt extinguishment, as this except from the Commercial Metals Company’s 2023 10-K shows:

These items are added back to net income in order to arrive at a measure of net operating profit after tax (NOPAT).

The Financial Accounting Standards Board (FASB) eliminated goodwill amortisation from 2002 and the International Accounting Standards Board (IASB) followed in 2005. Before that, goodwill, the capitalised value of the excess of purchase price over fair value of identifiable assets, required an annual charge to earnings for up to 40 years until the value of goodwill was eliminated. (Warren Buffett’s essay, “Goodwill and its Amortisation: The Rules and The Realities” in the appendix to his 1983 chairman’s letter, is an excellent discussion of goodwill amortisation). Since those accounting changes, goodwill is now subjected to impairment testing, which, unlike goodwill amortisation, is a real economic cost to the firm. Following “Core Earnings: New Data and Evidence” by Ethan Rouen, Eric So, and Charles C.Y. Wang, for years before the rule change, I add the goodwill amortisation charge to net income and for years after the rule change, the goodwill impairment charge, so as to arrive at a better measure of net operating profit after tax (NOPAT).

Effective 2005, the IASB required employee stock options (ESO) to be expensed in the income statement, with the FASB following a year later. Until then, firms could treat ESO compensation as if it was not a cost, inflating their reported earnings. Consequently, for the era before this accounting change, one must dig up data from the footnotes in order to calculate the cost of ESO issuances and ensure that results are comparable across periods and add the charge to net income so as to arrive at a better measure of NOPAT.

Under both IFRS and US GAAP, assets and liabilities held for sale are reported separately on the balance sheet and their income and loss from them, or the result of their sale, are reported as discontinued operations separate from continuing operations. This forms part of the business’ net income, adulterating the firm’s earnings.

In my pursuit of core profitability, I strip away the impact of income and losses from discontinued operations. For example, in its 2023 10-K, the Commercial Metals Company reported a $2.3 million gain on the sale of assets, and net earnings of $859.76 million. In order to properly estimate the recurring, and repeatable profitability of the business, it is necessary to remove this $2.3 million gain.

Because real estate investment trusts (REITs), by their nature, dispose of property, I do not perform the same exercise for REITs, choosing instead to incorporate such income and losses into my calculation of NOPAT.

While operational excellence should be the lodestar guiding managers, there is a great temptation to use reserves to manage earnings. In order to ward off the effects of earnings management, ensure comparability across business, and reveal timing of recurring cash flows from operations, the change in LIFO reserves, other inventory reserves and loan loss reserves year-over-year are added to my calculation of net operating profit after tax (NOPAT).

David Trainer, CEO and founder of New Constructs, notes that,

Loan loss provisions can be manipulated to boost a company’s earnings by bleeding off reserves. Or they can cause problems when companies need to “catch up” and take big provisions to raise reserves to more appropriate levels.

Fannie Mae (FNMA) had the largest change in total reserves of any company for the fiscal year 2012. FNMA decreased its loan-loss provision from $72 billion in 2011 to $59 billion in 2012, despite increasing its total amount of loans outstanding. Under GAAP rules, FNMA is able to boost earnings by the amount of decrease in reserves as income. Meanwhile, the 2012 loan loss provision was $9.4 billion less than actual charge-offs.

David Trainer, Change in Total Reserves – NOPAT Adjustment

Firms, in order to attract and retain talent, offer one of two kinds of retirement plans for their workers, the defined benefit plan, and defined contribution plan. A defined benefit plan, as the name suggests, guarantees a set benefit to its workers upon retirement. Firms may contribute or deduct more to or from this plan than is possible under a defined contribution plan. Defined benefit plans are the most complex and costly type of plan that businesses can set up and manage. Defined contribution plans, on the other hand, guarantee that a business will match an employee’s contribution and the employee receives regular payments during their retirement. This is the most popular kind of employer-sponsored plan in the United States.

In calculating net operating profit after-tax (NOPAT), one takes the costs or income of defined contribution plans as operating, and subtracts them from revenue. Defined benefit plans require more manipulation.

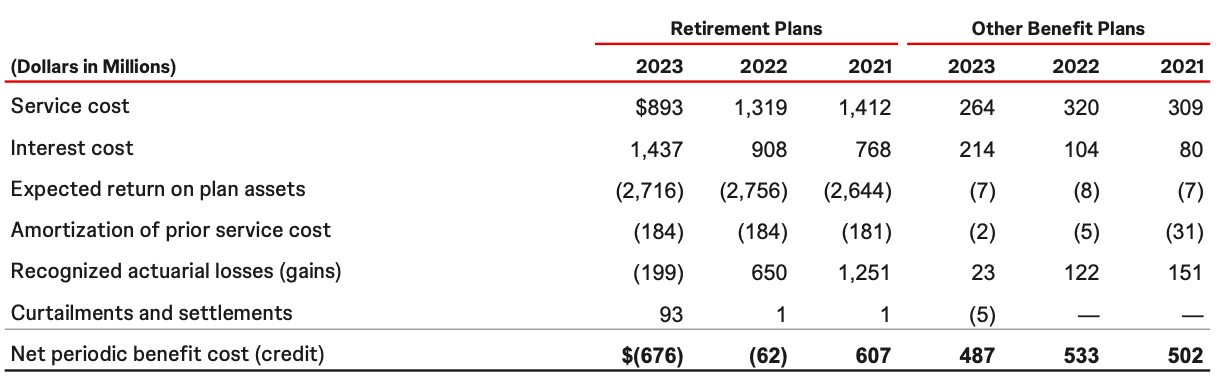

One of the themes of investing is that accounting standards are not written with equity investors as the primary audience, mixing operating and non-operating items, and so, disguising the true economics of a business. Pension accounting echoes this theme. The net periodic benefit cost (NPBC) of a defined benefit plan comes from both operating and non-operating elements. One must then analyse pension expenses line by line. An example from Johnson & Johnson’s 2023 10-K will provide a concrete example:

Service cost and the amortisation of prior service cost represent benefits granted to the employee in return for service to the company. Interest cost on plan liabilities, expected return on plan assets, and recognized gains and losses represent the evolution of plan assets and liabilities over time. If the change in plan assets matched the change in plan liabilities each year, these accounts would cancel. Since markets are volatile, this is not the case. As a result, the investment performance of plan assets contaminates pension expenses. Curtailments represent changes to the pension plan that restrict benefits.

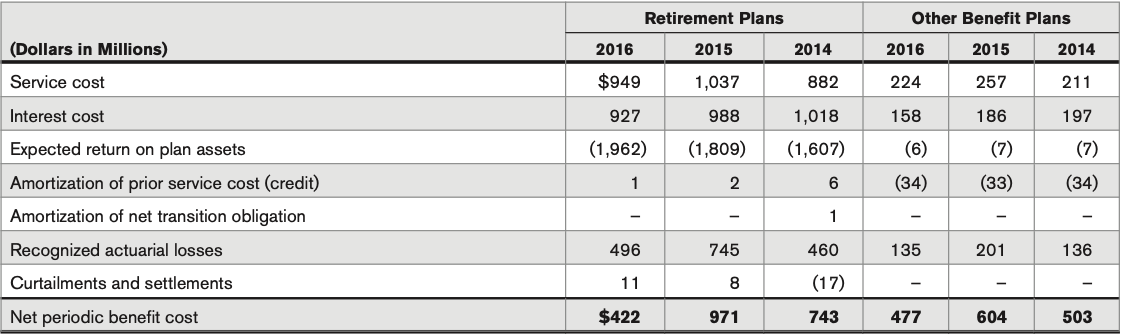

Before 2018, under Accounting Standards Codification (ASC) 715, firms reported the NPBC as an operating expense bundled under cost of sales and selling, general, and administrative (SG&A) expenses. Consequently, operating expenses and operating profit were tied to the performance of the firm’ plan assets. For example, in 2016, WK Kellogg Co. recognised a $304 million net loss on its plan assets, leading to a sharp increase in its pension expense to $199 million, and then in 2017, Kellogg recognised a $126 million net gain on its plan assets, leading to not only a $431 million benefit, but, because this was buried in cost of sales, the company’s operating profit rose from $1.4 billion to $1.95 billion. Accounting Standards Update (ASU) 2017-07, which went into effect in 2018, updating ASC 715, requires firms to

…report the service cost component in the same line item or items as other compensation costs arising from services rendered by the pertinent employees during the period. The other components of net benefit cost as defined in paragraphs 715-30-35-4 and 715-60- 35-9 are required to be presented in the income statement separately from the service cost component and outside a subtotal of income from operations, if one is presented. If a separate line item or items are used to present the other components of net benefit cost, that line item or items must be appropriately described. If a separate line item or items are not used, the line item or items used in the income statement to present the other components of net benefit cost must be disclosed.

Accounting Standards Update (ASU) 2017-07, Improving the Presentation of Net Periodic Pension Cost and Net Periodic Post-retirement Benefit Cost, FASB

This disaggregation of service costs from the other components of NPBC reflects the Financial Accounting Standards Board’s (FASB) consideration that service costs are the only operating component of NPBCs. This is because service costs are the one component of NPBC that represents an annual compensation cost, and, therefore, not only is it reported within operating income, it also forms a part of my calculation of net-operating profit after tax (NOPAT). Whereas FASB considers amortisation of prior service cost as an non-operating expense, I treat it as an operating expense for historical benchmarking purposes, but because FASB considers this a non-operating expense, I adjust to reflect my own standards. When net benefit obligations decline, service costs are a net gain, and are treated as non-operating items and so, do not form a part of my calculation of NOPAT. The same logic applies to amortisation of prior service costs. These two are the only components of my calculation of NOPAT.

Interest cost, expected return on plan assets, and recognized gains and losses, treated as operating items before 2018, are now disclosed as non-operating items. Settlements and curtailments, which were inconsistently disclosed prior to 2018, are now disclosed as non-operating items. The impact of these non-operating items must be stripped away from any calculation of NOPAT, both prior to 2018 and after 2018. It must be said that, for reports prior to 2018, one has to read the footnotes and management discussion & analysis (MD&A) to verify, where possible, whether recurring items such as interest costs are indeed buried within operating expenses, and whether non-recurring items such as curtailments and settlements, are buried within operating or non-operating expenses. For example, in 2016, in their annual report, Johnson & Johnson broke down their NPBC as follows:

Curtailments and settlements were reported as non-operating items, and so, in order to determine the impact of non-operating NPBC on operating expenses, the appropriate calculation would be the following, which gives a $252 million increase in operating expenses:

Non-operating income is the complement of non-operating expenses, and are special items and one-time earnings that are not reported on the face of the income statement, and are instead hidden in other line items. The most common types of hidden non-operating expenses are gains on the sale of assets, some pension income, and income from legal settlements.

An example of non-operating income is the unusually large gain on property sale, $600 million, that Alexander’s Inc., a real estate investment trust (REIT), received in 2012, which was 89% of its $674 million GAAP income, as reported in the REIT’s 2012 10-K:

Non-operating expenses, such as asset write-downs, which I discussed in a separate post, are special items and one-time charges that are not reported on the face of the income statement, and are instead hidden in other line items. The most common types of hidden non-operating expenses are litigation charges, restructuring costs, amortization of acquired intangibles, some pension costs, and losses on asset sales. An example of a non-operating expense hidden in operating earnings is the $5 billion penalty that Meta Platforms paid as part of a settlement with the Federal Trade Commission (FTC) and which the company reported on page 22 of its 2019 10-K:

Academic research has investigated the persistence and predictability of these expenses, and, although nearly research found that year-on-year persistence and predictability was hard to discern, more recent research has found that across many years, there is persistence of special items for firms with strong core profits. Simply, firms with strong core profits and which report a series of restructuring charges, for example, are likely to do so in future, as Meta Platforms’ has done in recent years, whereas firms with low core profitability, are unlikely to repeat the trick. Researchers believe this is because firms may shift operating items into special items in order to manage their earnings. However, it is difficult to extend this research to any meaningful conclusions about individual companies.