Net Deferred Tax Assets and Liabilities, a Valuation Adjustment

Deferred tax accounts arise because of differences in how firms and the government account for taxes. For example, whereas the government uses accelerated depreciation to calculate taxes owed, firms employ straight-line depreciation. The taxes the company will actually pay, its “cash taxes”, will be lower than the tax expense or provision for income taxes that it will report.

When the business’ reported income is less than its taxable income, the firm generates deferred tax assets (DTAs), whereas when its reported income is greater than its taxable income, deferred tax liabilities (DTLs) are created. They are either reported on the face of the balance sheet, or off its face, hidden away in the notes. DTAs increase a firm’s reported assets, whereas, DTLs can be seen as a kind of interest-free debt.

“Deferred Tax Assets and Liabilities, an Invested Capital Adjustment”, Joseph Noko

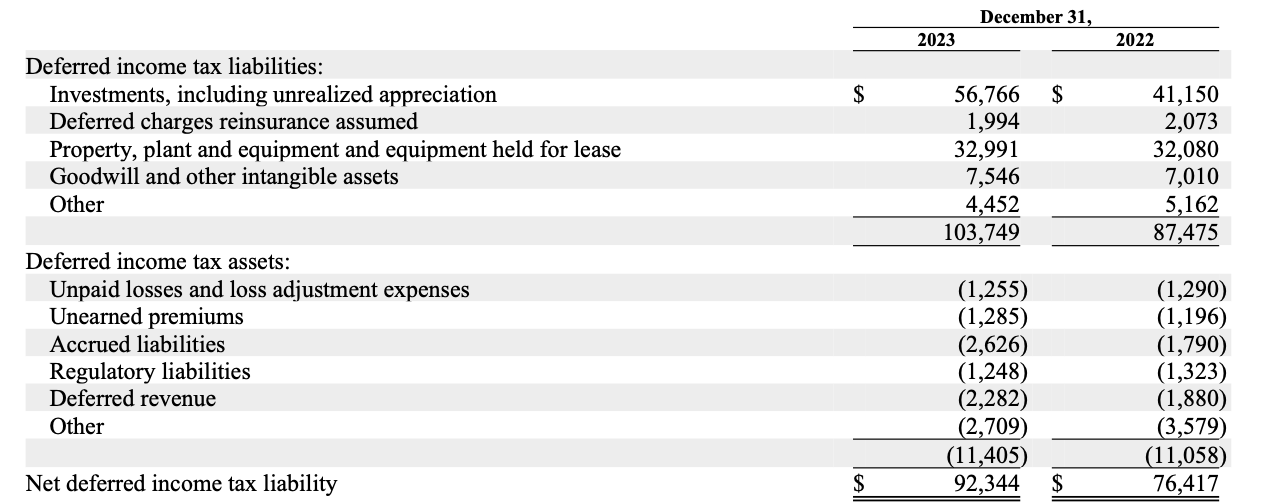

In my calculation of economic book value (EBV), I deduct DTLs, net of DTAs because they are real obligations that will have to be paid in future, reducing shareholder value. DTAs, net of DTLs, on the other hand, are not added to EBV because they cannot be converted into shareholder value, by selling them, for example, and, because they do not represent real value. The most famous example of net DTLs is Berkshire Hathaway, who, in page K-103 of their 2023 annual report, disclosed net DTLs of $92.34 billion.