This Statement improves financial reporting by requiring an employer to recognize the overfunded or underfunded status of a defined benefit postretirement plan (other than a multiemployer plan) as an asset or liability in its statement of financial position and to recognize changes in that funded status in the year in which the changes occur through comprehensive income of a business entity or changes in unrestricted net assets of a not-for-profit organization. This Statement also improves financial reporting by requiring an employer to measure the funded status of a plan as of the date of its year-end statement of financial position, with limited exceptions.

Summary of Statement No. 158, Financial Accounting Standards Board (FASB)

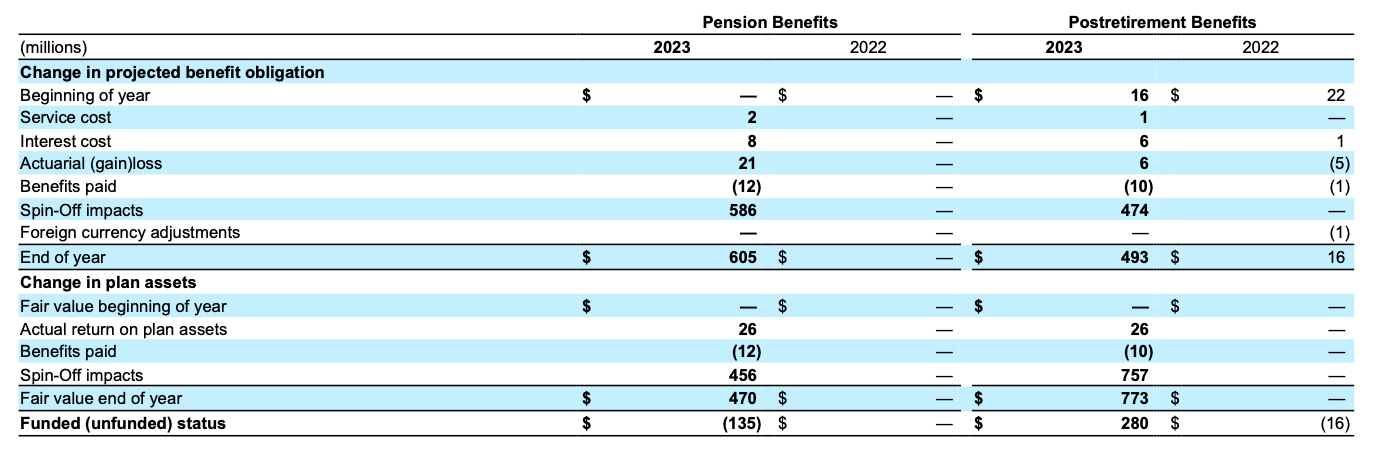

When retirement-related assets and liabilities are too small to disclose on the face of the balance sheet, companies will often elect to include prepaid pension assets within long-term assets and unfunded pension liabilities in other long-term liabilities, disclosing the details in the notes. For example, W.K. Kellogg, in its 2023 10-K, provided the details of its retirement-related assets and liabilities in note 9, “Pension and Post-Retirement Benefits”, starting on page 70. In 2023, the company had around $1.1 billion in pension and post-retirement benefits, against plan assets valued at $1.24 billion, for a net funded status of $145 billion.

The $145 million in excess funds tied up in the plan assets are given the same treatment as excess cash and do not form a part of the invested capital calculation. Instead, that $145 million is dedicated from my invested capital calculation, because it is not needed to generate any returns, it is dead capital. On the other hand, underfunded plans are effectively borrowings from the employees, and do not require any adjustments to invested capital calculation.