Firms, in order to attract and retain talent, offer one of two kinds of retirement plans for their workers, the defined benefit plan, and defined contribution plan. A defined benefit plan, as the name suggests, guarantees a set benefit to its workers upon retirement. Firms may contribute or deduct more to or from this plan than is possible under a defined contribution plan. Defined benefit plans are the most complex and costly type of plan that businesses can set up and manage. Defined contribution plans, on the other hand, guarantee that a business will match an employee’s contribution and the employee receives regular payments during their retirement. This is the most popular kind of employer-sponsored plan in the United States.

In calculating net operating profit after-tax (NOPAT), one takes the costs or income of defined contribution plans as operating, and subtracts them from revenue. Defined benefit plans require more manipulation.

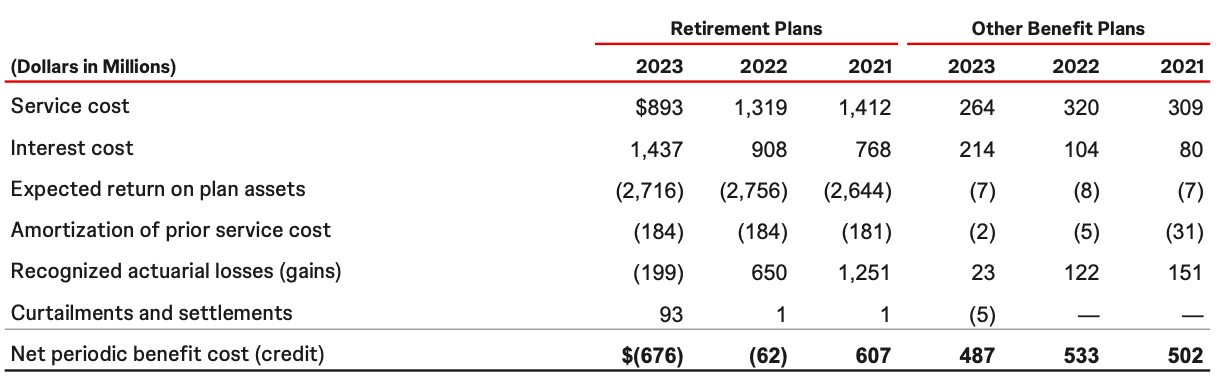

One of the themes of investing is that accounting standards are not written with equity investors as the primary audience, mixing operating and non-operating items, and so, disguising the true economics of a business. Pension accounting echoes this theme. The net periodic benefit cost (NPBC) of a defined benefit plan comes from both operating and non-operating elements. One must then analyse pension expenses line by line. An example from Johnson & Johnson’s 2023 10-K will provide a concrete example:

Service cost and the amortisation of prior service cost represent benefits granted to the employee in return for service to the company. Interest cost on plan liabilities, expected return on plan assets, and recognized gains and losses represent the evolution of plan assets and liabilities over time. If the change in plan assets matched the change in plan liabilities each year, these accounts would cancel. Since markets are volatile, this is not the case. As a result, the investment performance of plan assets contaminates pension expenses. Curtailments represent changes to the pension plan that restrict benefits.

Valuation: Measuring and Managing the Value of Companies, Tim Koller, Marc Goedhart, and David Wessels

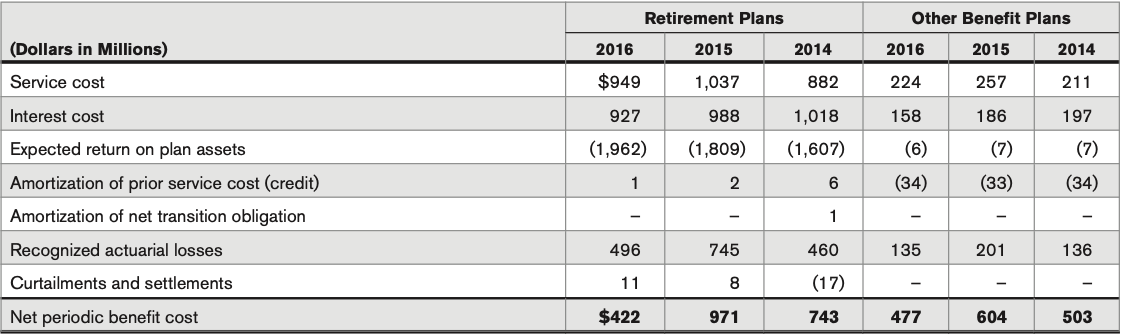

Before 2018, under Accounting Standards Codification (ASC) 715, firms reported the NPBC as an operating expense bundled under cost of sales and selling, general, and administrative (SG&A) expenses. Consequently, operating expenses and operating profit were tied to the performance of the firm’ plan assets. For example, in 2016, WK Kellogg Co. recognised a $304 million net loss on its plan assets, leading to a sharp increase in its pension expense to $199 million, and then in 2017, Kellogg recognised a $126 million net gain on its plan assets, leading to not only a $431 million benefit, but, because this was buried in cost of sales, the company’s operating profit rose from $1.4 billion to $1.95 billion. Accounting Standards Update (ASU) 2017-07, which went into effect in 2018, updating ASC 715, requires firms to

…report the service cost component in the same line item or items as other compensation costs arising from services rendered by the pertinent employees during the period. The other components of net benefit cost as defined in paragraphs 715-30-35-4 and 715-60- 35-9 are required to be presented in the income statement separately from the service cost component and outside a subtotal of income from operations, if one is presented. If a separate line item or items are used to present the other components of net benefit cost, that line item or items must be appropriately described. If a separate line item or items are not used, the line item or items used in the income statement to present the other components of net benefit cost must be disclosed.

Accounting Standards Update (ASU) 2017-07, Improving the Presentation of Net Periodic Pension Cost and Net Periodic Post-retirement Benefit Cost, FASB

This disaggregation of service costs from the other components of NPBC reflects the Financial Accounting Standards Board’s (FASB) consideration that service costs are the only operating component of NPBCs. This is because service costs are the one component of NPBC that represents an annual compensation cost, and, therefore, not only is it reported within operating income, it also forms a part of my calculation of net-operating profit after tax (NOPAT). Whereas FASB considers amortisation of prior service cost as an non-operating expense, I treat it as an operating expense for historical benchmarking purposes, but because FASB considers this a non-operating expense, I adjust to reflect my own standards. When net benefit obligations decline, service costs are a net gain, and are treated as non-operating items and so, do not form a part of my calculation of NOPAT. The same logic applies to amortisation of prior service costs. These two are the only components of my calculation of NOPAT.

Interest cost, expected return on plan assets, and recognized gains and losses, treated as operating items before 2018, are now disclosed as non-operating items. Settlements and curtailments, which were inconsistently disclosed prior to 2018, are now disclosed as non-operating items. The impact of these non-operating items must be stripped away from any calculation of NOPAT, both prior to 2018 and after 2018. It must be said that, for reports prior to 2018, one has to read the footnotes and management discussion & analysis (MD&A) to verify, where possible, whether recurring items such as interest costs are indeed buried within operating expenses, and whether non-recurring items such as curtailments and settlements, are buried within operating or non-operating expenses. For example, in 2016, in their annual report, Johnson & Johnson broke down their NPBC as follows:

Curtailments and settlements were reported as non-operating items, and so, in order to determine the impact of non-operating NPBC on operating expenses, the appropriate calculation would be the following, which gives a $252 million increase in operating expenses: