The reader should read this post in conjunction with a Google spreadsheet I have created on Meta Platforms’ operating, variable, and not-yet commenced leases. If wealth, as I contend, tends toward destruction in the long run, an investor has two choices: not to invest, or, to do something that shifts the odds in one’s favour. One of these things is to make a rigorous examination of a company’s reports, and make the appropriate adjustments to understand the true state of the economics of a business. This post discusses operating leases and their impact on my calculation of both NOPAT and invested capital.

Operating Leases

Since 2019, the International Accounting Standards Board’s (IASB) IFRS 16, “Leases,” and the Financial Accounting Standards Board’s (FASB) Accounting Standards Update (ASU) 2016-02, “Leases” (Topic 842), have been in effect, obliging companies to capitalise all their operating leases, which are contractual obligations under which a firm uses an asset without owning it, unlike finance leases, which are a form of debt that bestows ownership benefits to the leasee. Prior to these changes, operating leases and the value of the leased asset were not recorded on the balance sheet, and only a rental expense was recorded on the income statement, disguising the indebtedness of the business and scale of assets operated, giving them a more hallowed appearance compared to firms that had bought assets using debt, who had to record the value of the debt incurred and the asset bought on its balance sheet, and the related interest expense and depreciation on the income statement.

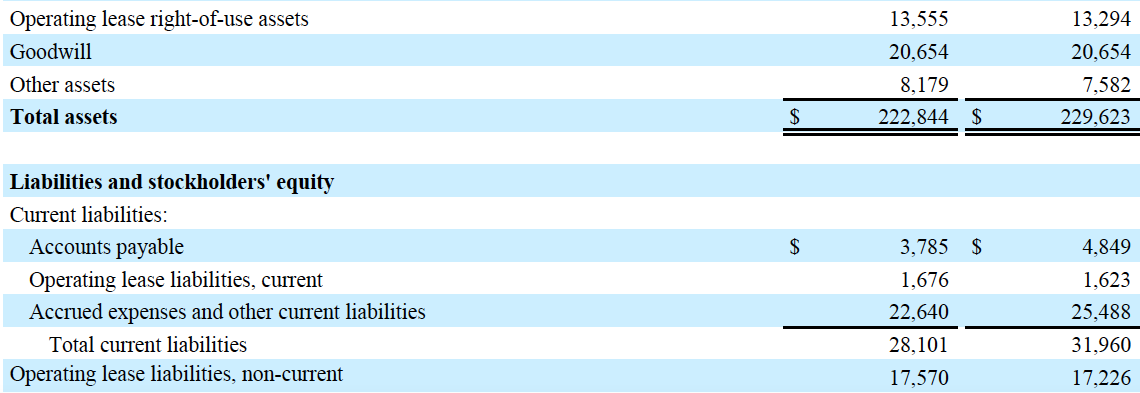

On the balance sheet, firms have to record the present value of the operating lease payments, or lease liability, as a single line item, or bundle it with other current and long-term liabilities; and a right-of-use asset line item, as shown in the except from Meta Platforms’ 1Q 2024 10-Q below and which represents the firm’s right to use the underlying asset, or bundle that asset within property, plant and equipment (PP&E), or other assets. A firm may choose to record a single lease liability, bundling operating and finance leases, breaking them out in the notes.

On the income statement, under International Financial Reporting Standards (IFRS), operating lease payments are recorded within depreciation and interest expense, and under Generally Accepted Accounting Principles (GAAP), the entire lease expense, including embedded interest, is recorded under operating expenses such as cost of sales.

Accounting statements filed before 2019 were not adjusted to reflect these new standards, and so I adjust them to include operating leases. This requires scouring the notes to find the future operating lease payments, adding the total undiscounted cash flows, and discounting them by a standardised cost of debt. Firms use an internally derived discount rate to capitalise their operating leases. There is a rate implicit in the lease (RIIL) which requires information that lessees typically do not have, and so, firms will usually use a collateralized incremental borrowing rate (IBR). Given that firms issue uncollateralised debt, calculating an estimate of collateralized IBR is a quite difficult thing to do. Using this rate, companies are able to estimate the present value of their operating lease obligations. In order to strip away the effect of idiosyncratic and perhaps adulterated assumptions that go into calculating collateralized IBR, I use the yield to maturity on AA-rated corporate debt as a discount rate across all US-domiciled firms, and an equivalent measure in other jurisdictions, reflecting the liquidity of operating leases.

The present value of operating leases is added to my measure of invested capital. The implied interest is simply the present value of the operating lease obligations multiplied by the cost of debt. This will be deducted from my calculation of NOPAT to give an unlevered measure of core operating profitability. As it is a form of debt, in my calculation of shareholder value, I subtract operating lease liabilities from enterprise value.

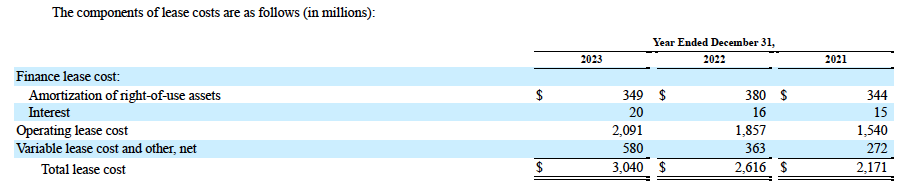

For the post-2019 era, for the sake of consistency, I calculate operating lease liabilities and implied interest according to the method I have described, removing the operating lease debt from the balance sheet and replacing it with a total operating lease adjustment, which is the difference between my calculation of the present value of operating leases and the firm’s reported value. In instances such as the one below, taken from Meta Platforms’ 2023 10-K, where the operating lease cost is given in one line-item, I deduct my measure of implied interest expense from operating expense, and where the interest expense is disclosed, I may consider this measure in its stead.

Variable and Not-Yet Commenced Leases

The impact of variable and not-yet-commenced leases remains off the face of the financial statements, as discussed in the paper, Variable Leases Under ASC 842: First Evidence on Properties and Consequences. This is because operating leases need only be recorded on the balance sheet when a contract has been signed, payments have commenced and the firm has begun using the underlying asset.

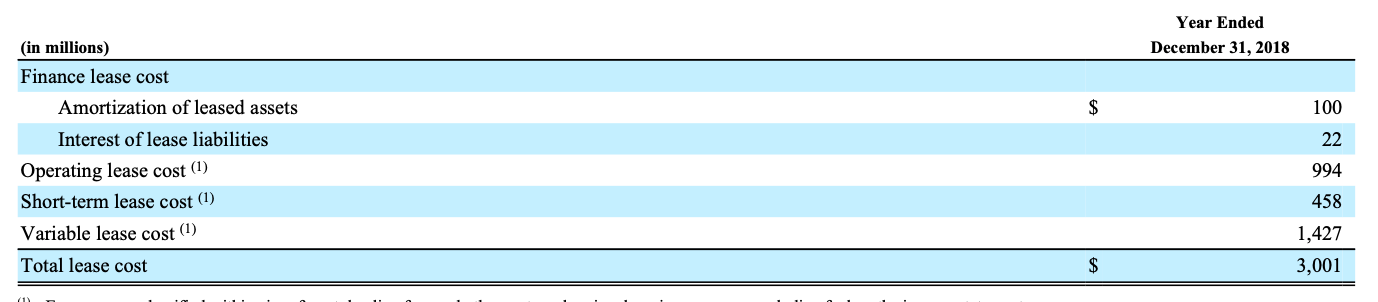

If leases have variable payments, they may be excluded from the operating lease calculation, given the supposed difficulty of reliably forecasting them due to changes in the economic activity tied to the leased asset. However, these leases can be rather large. In 2018, for example, variable leases were 48% of Delta’s total lease costs, 54% of American Airlines’, 69% for United Airlines, and 77% for Southwest Airlines’.

Moreover, under IFRS 16 and ASU 2016-02, firms are obliged to report on leases that have been agreed to, create material obligations, but have yet to commence. Like variable leases, not-yet commenced leases are not considered a part of operating lease obligations. For instance, Meta Platforms reported $7.07 billion in not-yet commenced operating leases, on page 111 of its 2023 10-K. Consequently, to have a fuller picture of the obligations firms are under, include both variable and not-yet commenced leases in my calculation of a firm’s present value of future operating lease payments.

Variable Lease Expense

To calculate the impact of variable leases, I multiply the standardised present value of operating leases by Variable Lease Expense/Operating Lease Expense. This number is then added to the present value of operating leases. For example, Meta Platforms reported $580 million in variable lease cost, on page 110 of its 2023 10-K, and an operating lease cost of $2.091 billion. This gives us a multiplier of 0.28, which multiplies my standardised present value of operating leases to calculate the present value of variable leases. This is added to my standardised present value of operating leases. Variable leases were responsible for 17.6% of Meta Platforms’ total operating leases.

Not-Yet-Commenced Lease Expense

To calculate the impact of not-yet commenced leases, I multiply the standardised present value of operating leases by Not -Yet-Commenced/Total Lease Payments. This number is then added to the present value of operating leases. For example, we showed above that in 2023, Meta Platforms had $7.07 billion in not-yet commenced leases, which is divided by $23.649 billion in total lease payments, to give a multiplier of 0.30. This multiplier acts upon the standardised present value of operating leases to give a present value of not-yet commenced leases. This is also added to the standardised present value of operating leases. Not-yet commenced leases were responsible for 19% of Meta Platforms’ total operating leases.