In a period of regime uncertainty, JPMorgan Chase & Co. (JPM: $288.19/share) is not only a paradigmatic bank, with a history of profitability stretching back decades,and a “fortress balance sheet”, it is also an attractive investment opportunity.

Banking in a Fuzzy Zone

Since the Great Recession, termed, “largely unprecedented and virtually inconceivable“ by JP Morgan Chase & Co Jamie Dimon, banking has undergone profound changes, with a wave of bankruptcies, government bailouts and nationalisations, and restructuring and industry consolidation in terms of branch deposits, and increasing competition in terms of lending. Regulators, in the United States, the Federal Reserve, along with the Office of the Comptroller of the Currency (OCC) and the Federal Deposit Insurance Corporation (FDIC), have intensified bank regulations, with more stringent capital requirements, greatly curtailed trading operations, and, in Europe, caps on bonuses. The ongoing “Basel III Endgame” proposal, opposed by the American Bankers Association (ABA), seeks to further increase capital requirements, particularly for larger banks. Although the initial proposal for a 16-19% increase has been revised downwards to around 9% for the largest banks, this still represents a substantial increase in the “capital buffer.”

Since 2018, U.S. banks have benefited from the country’s stellar economic growth, attendant burgeoning loan demand, and a decline in bad debts, that has allowed them to outstrip their pre-crisis profit levels, compared to a Europe that Dimon recently warned is “losing”. Events in 2024, an unfolding of regime uncertainty, has benefitted European bank valuations, even if European fundamentals have not meaningfully improved compared to the United States. Banking is in a fuzzy zone between boom and bust, in which regulatory constraints have served to discipline the market. Although the collapse of the Silicon Valley Bank, Signature Bank, and First Republic Bank and the emergence of banks-as-synthetic-hedge-funds, has exposed the profitability challenges of small and regional banks; although the non performing loans ratio has increased modestly; although the prospect of interest rate cuts threatens net interest margins (NIM), on the rise since Q1 2024, given the relationship between the two; although loan demand is weakening; the Federal Reserve has concluded that, “large banks are well positioned to weather a severe recession, while staying above minimum capital requirements and continuing to lend to households and businesses”.

Profiting Across Cycles

JPMorgan Chase has been a beneficiary of the tailwinds of the post-Great Recession world, while prudently managing the risks of that period. A consequence of this success is that, since 2019, the bank’s operating revenue has swelled from $142.42 billion to $281.51 billion in the last twelve months (LTM), compounding at a rate of 12.03% a year. The bank’s 5-year sales CAGR, at 16.8%, compares very favourably to a 6.9% mean and 5.2% median for the world’s 1,000 largest firms. In that time, the bank’s net operating profit after tax (NOPAT) has ballooned from $34.18 billion to $60.06 billion, compounding at a rate of 9.85%.

With rising profitability has come copious amounts of free cash flow (FCF), with the firm generating $$171.17 billion in FCF since 2021, equivalent to 21.37% of its current market cap. With $50.35 billion in FCF in the LTM grants it an attractive 6.17% FCF yield.

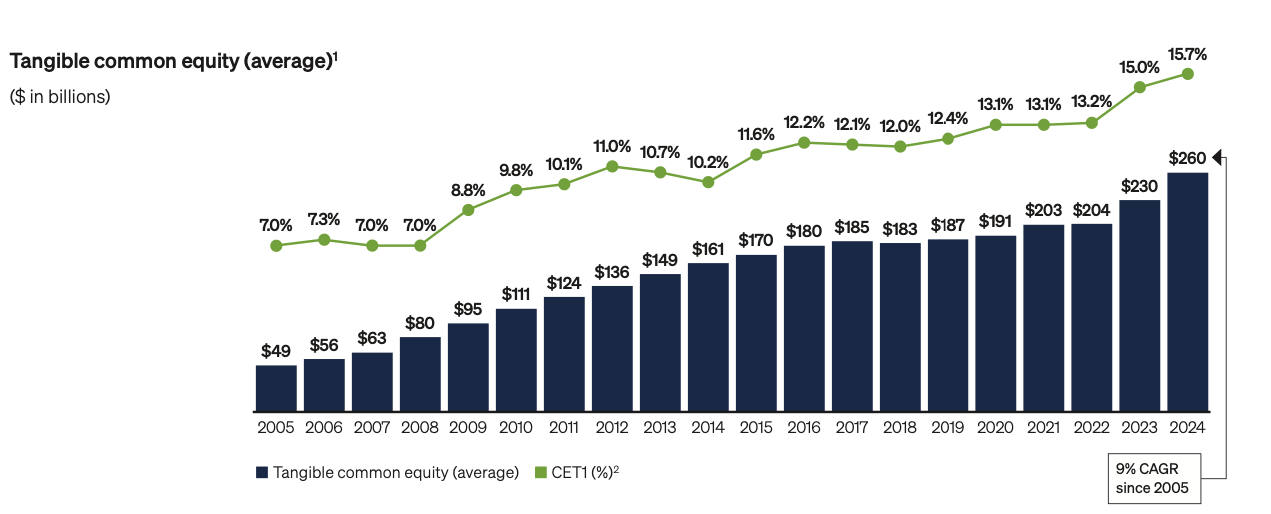

Prepared for Severe Adversity

The bank’s “fortress balance sheet” has continually been reinforced under Dimon’s stewardship. As of the end of Q1 2025, the bank’s Common Equity Tier 1 (CET1) was $280 billion, with a Standardized CET1 capital ratio of 15.4%, compared to 15% in Q1 2024, and 15.7% at the end of 2024.

JPMorgan Chase’s recently disclosed results from its 2025 Annual Dodd-Frank Act Stress Test projected financial resilience under the Federal Reserve’s Supervisory Severely Adverse Scenario, which hypothesises a severe global recession accompanied by substantial stress in commercial and residential property markets and corporate debt markets over a nine-quarter period from 1Q 2025 to 1Q 2027. Under this extraordinarily challenging scenario, characterised by a 7.8% decline in U.S. GDP, unemployment reaching 10%, a 50% stock market decline, and 33% fall in house prices, the bank’s Common Equity Tier 1 capital ratio would decline from 15.7% to a minimum of 13.7%, whilst still maintaining comfortable margins above regulatory minima. The stress test projects cumulative pre-provision net revenue of $93.8 billion offset by $79.3 billion in credit loss provisions and $12.4 billion in trading and counterparty losses, resulting in a modest net loss before taxes of $3.2 billion over the entire nine-quarter period. Notably, the bank’s capital position would remain robust throughout the hypothetical crisis, with all key capital ratios, including the Supplementary Leverage Ratio maintaining a minimum of 5.6%, demonstrating the bank’s fundamental strength and capacity to continue serving clients even under severely adverse economic conditions.

Moreover, the bank’s catastrophic loss-absorbing capacity is impressive, with JPMorgan Chase boasting a Total Loss-Absorbing Capacity (TLAC) (see page 106 of the 2024 annual report for a detailed explanation) of $558.3 billion as of Q1 2025, 30.8% of risk-weighted assets (RWA), compared to a regulatory requirement of 23%, indicating a $140.8 billion surplus. TLAC is 11.3% of total leverage exposure, compared to a 9.5% regulatory requirement, indicating an $87.7 billion surplus.

Upside Remains

At the current price, $288.19 at time of writing, JPMorgan Chase trades at a price-to-economic book value (PEBV) of 1.25, its highest ever level in my analysis window. This implies that the market expects the bank to grow its NOPAT by 25% from current levels. Using my reverse discounted cash flow (DCF) model, I unearthed the cash flow expectations implied by the current price.

In the first scenario, I determined the conditions under which the firm’s share price is justified, wherein,

- Revenue grows by 7.1% in 2025, 2.6% in 2026, and 3.9% in 2027, in line with consensus estimates, and by 16.8% thereafter, and,

- NOPAT margin remains at 21.33%

In this scenario, NOPAT compounds by an average of 4.11% a year, and the firm has an attractive market-implied competitive advantage period (MICAP) of four years in which the shareholder value per share equals the current stock price.

If, on the other hand,

- Revenue grows by 16.8% a year, and,

- NOPAT margin remains at 21.33%.

Then the stock is worth $404.75, an upside of 40.45% from the current price.

If,

- Revenue grows by 12.71% a year, the 3-year CAGR, and,

- NOPAT margin remains at 21.33%.

Then the stock is worth $337.31, an upside of 17.04% from the current price.