Under both IFRS and US GAAP, assets and liabilities held for sale are reported separately on the balance sheet and their income and loss from them, or the result of their sale, are reported as discontinued operations separate from continuing operations. This forms part of the business’ net income, adulterating the firm’s earnings.

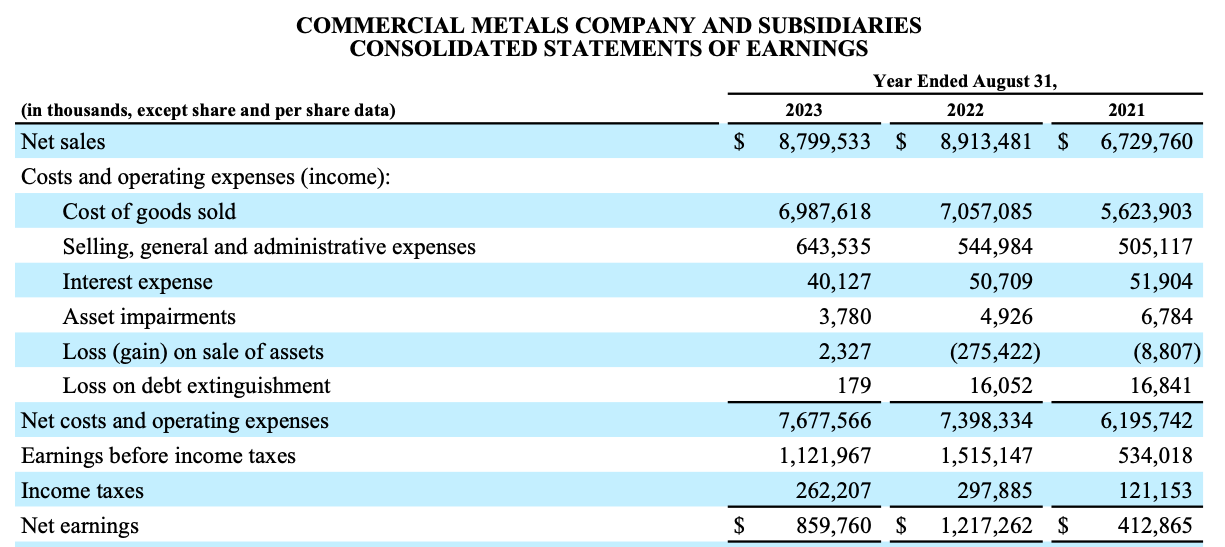

In my pursuit of core profitability, I strip away the impact of income and losses from discontinued operations. For example, in its 2023 10-K, the Commercial Metals Company reported a $2.3 million gain on the sale of assets, and net earnings of $859.76 million. In order to properly estimate the recurring, and repeatable profitability of the business, it is necessary to remove this $2.3 million gain.

Because real estate investment trusts (REITs), by their nature, dispose of property, I do not perform the same exercise for REITs, choosing instead to incorporate such income and losses into my calculation of NOPAT.